Question for SCOTUS: How Do Shareholders “Realize” Firms’ Retained Earnings??

Question for SCOTUS: How Do Shareholders “Realize” Firms’ Retained Earnings??

Simplifying Moore vs United States

I won’t recount every detail of this case, just argued before the Supreme Court. Let’s cut to the chase.

There are two tax treatments in the U.S. for corporate earnings: C-corps, and all the others, which are all “pass-throughs.” C-corps pay tax on their profits/“net earnings,” and their shareholders also pay taxes on any portion of those earnings that are distributed as dividends. With pass-throughs (S-corps, partnerships, LLCs, and sole proprietorships), the shareholders pay taxes on the full corporate profits every year, whether they’re distributed or not. They “own” those profits, after all, whether they’re in shareholders’ bank accounts, or held in the company that they own.

The company at issue in Moore is a pass-through. It made profits, and the IRS says they’re taxable for shareholders, in normal manner for pass-throughs.

So why are the plaintiffs fussing about those retained earnings being “capital gains” that haven’t been “realized” by the shareholders?

Understand: the only way shareholders could “realize retained earnings” is if there’s a share buyout, where all the shareholders can sell their shares at some higher price than they paid, thus “realizing” the dollar value that had been “retained” inside the company they own.

But wait. Does this mean that the undistributed profits/retained earnings of any pass-through are “unrealized” so untaxable absent a share buyout? Would pass-throughs’ shareholders then only pay taxes on distributed profits, while (unlike C-corps) neither shareholders nor the pass-through pay any taxes on undistributed profits?

Words matter. The twisted pretense that retained profits/earnings can be “realized” (versus distributed) creates this whole dumpster fire of a controversy. It’s standard-issue legalistic, terminological hand-waving and legerdemain, the M.O. for the ownership class from time immemorial. Realization is immaterial to the question at hand.

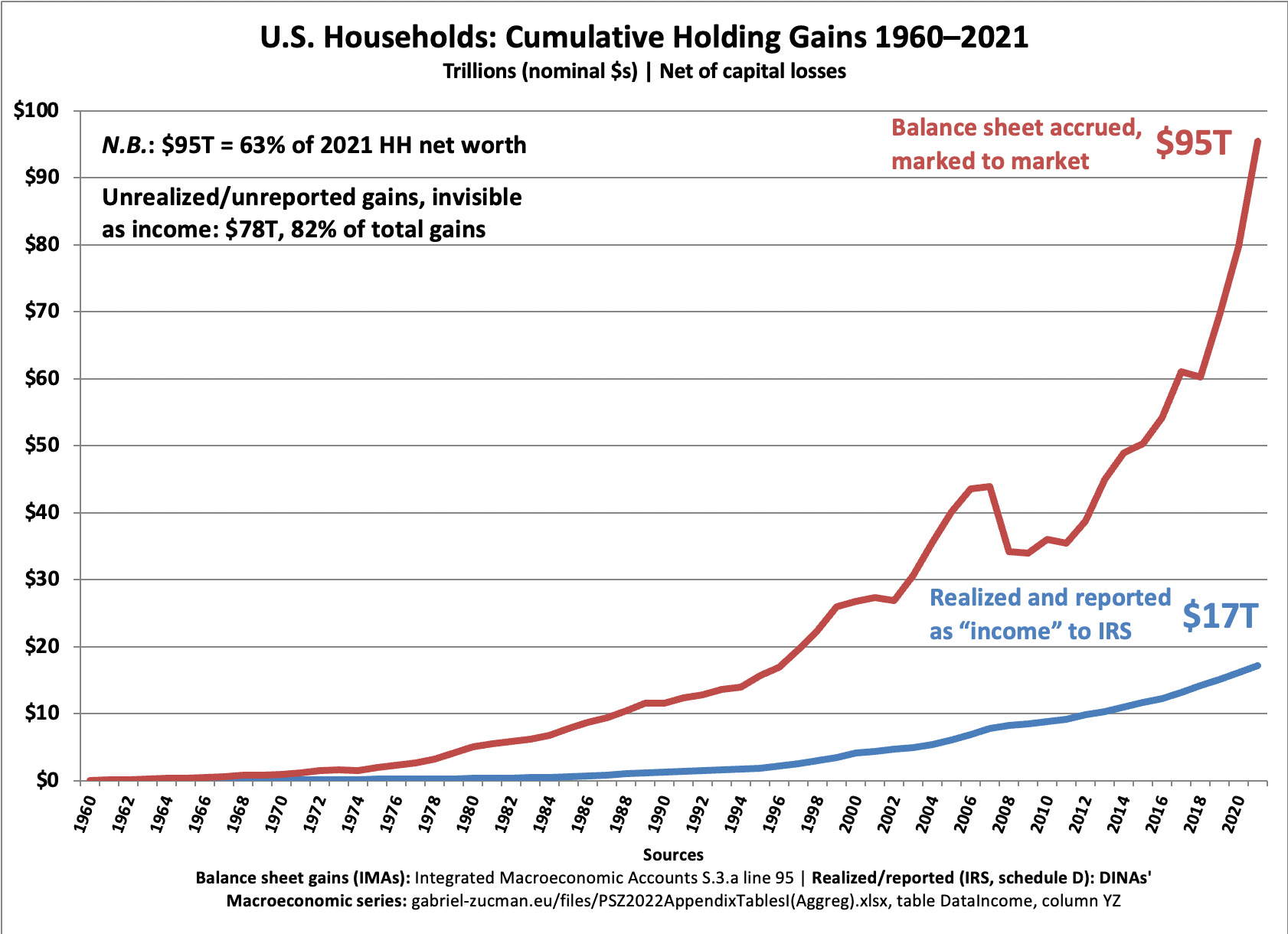

Meanwhile, consider how cap-gains taxation actually does work: shares in your portfolio go up and up in price (long term at least), and those gains are part of the “total return” every portfolio holder looks at whenever they hop on their brokerage site to evaluate their investments’ performance. But you only pay taxes on those gains if you “realize” them by swapping shares for cash with some other portfolio holder (sell them). The year-in-and-year-out gains prior to that are…simply ignored as “income.”

To keep things short and simple, here’s how that’s played out over six decades for U.S. households.

Sweet deal for shareholders huh?

As always: Very interesting thoughts and graphics! But I am not completely sure I understand all of what you are writing.

When someone bought a share A in January 2023 for 100 $ and sells it in Mai of 2023 for 150 $ he doesn’t pay any taxes on that. If he then bought in August of 2023 a share B for 150 $ that is worth 180 $ at the end of the year 2023 he has to pay capital gains taxes on the 30 $?